The global transition away from LIBOR

What's happening?

Regulators called for the global financial industry to transition away from the London Interbank Offered Rate, also known as LIBOR to new alternative reference rates (ARRs).

LIBOR is a set of benchmark interest rates that major global banks use to price a wide range of products, including corporate loans, derivatives, residential mortgages, student loans, corporate bonds, and other securities.

SVB is committed to helping you understand the new rates and how these changes may impact your loan or other products in the future.

SVB will continue to navigate through the industry cessation of LIBOR and on to the new ARRs, and will focus on migrating all remaining LIBOR-based deals throughout 2022.

Please refer to the FAQs below for more information about the transition away from LIBOR. For further detail on how the transition away from LIBOR may impact you specifically, please discuss with your financial and legal advisors.

SVB now offers alternative reference rates globally

The end of 2021 saw cessation of nearly all global LIBOR rates including the 1-week and 2-month USD LIBOR tenors. SVB is prepared to offer products tied to ARRs for clients today across USD (SOFR), GBP (SONIA), and EUR (€STR).

For USD loans, SVB supports Term SOFR (1-,3-,6-month tenors) and Daily Simple SOFR conventions. In 2022, focus will be on legacy contracts and continued migration away from LIBOR to ARRs.

| Cessation Date | Proposed ARR | SVB Supported Conventions | |

|---|---|---|---|

| USD LIBOR | 12/31/2021 1-week & 2-month tenors 6/30/2023 overnight, 1-,3-,6- & 12-month tenors |

Secured Overnight Financing Rate (SOFR) | Term SOFR (1-, 3-, and 6-month tenors) Daily Simple SOFR |

| GBP LIBOR | 12/31/2021 | Sterling Overnight Index Average (SONIA) | SONIA Compounded Daily in Arrears |

| Euro LIBOR (Not Euribor) | 12/31/2021 | Euro Short-term Rate (€STR) |

€STR Compounded in Arrears |

A number of important LIBOR transition-related announcements were released on March 5, 2021, by the UK Financial Conduct Authority (FCA) and approved by the Alternative Reference Rates Committee (ARRC), relating to confirmation of the cessation dates for LIBOR and spread adjustments.

These announcements serve to fix the spread adjustment to be used for clients migrating under the industry standard fallback language; and are intended to accelerate market participants’ move away from LIBOR.

The fixing of the spread adjustment provides an economic basis from which to transition LIBOR to SOFR on existing deals. Further information will be provided to clients with existing products having LIBOR pricing over the coming months.

Background

These announcements serve to cease publication of the following LIBOR tenors:

Cessation of LIBOR rates

(i) all GBP, EUR, CHF and JPY LIBOR settings, and the 1 Week and 2 Month USD LIBOR settings immediately following the LIBOR publication on December 31, 2021; and

(ii) the Overnight and 1, 3, 6 and 12 Month USD LIBOR settings immediately following the LIBOR publication on June 30, 2023.

Where can I find additional information?

We will continue to update this page as new information is received. SVB clients may submit questions to the email address on this page and/or reach out to your relationship manager with any questions you may have.

Please see below for links to statements and press releases from the FCA, ISDA, IBA, and Bloomberg.

Links to statements

FCA press release: FCA Announcements on the end of LIBOR- ISDA press release: ISDA Statement on UK FCA LIBOR Announcement

- IBA release: ICE Benchmark Administration Publishes Feedback Statement for the Consultation on Its Intention to Cease the Publication of LIBOR Settings

- Bloomberg announcement: IBOR Fallbacks Announcement - Spread Fixing Event from LIBOR

FAQs

What is LIBOR?

Why is LIBOR going away?

What does this transition mean for SVB clients?

What is SVB doing to prepare?

SVB has established a transition team to manage the transition for SVB clients and provide oversight. SVB also has representation in the ARRC, and our transition team is taking action to meet planned milestones. As the transition evolves and we develop guidelines and protocols for contracts and product offerings, we’ll continue to update our clients.

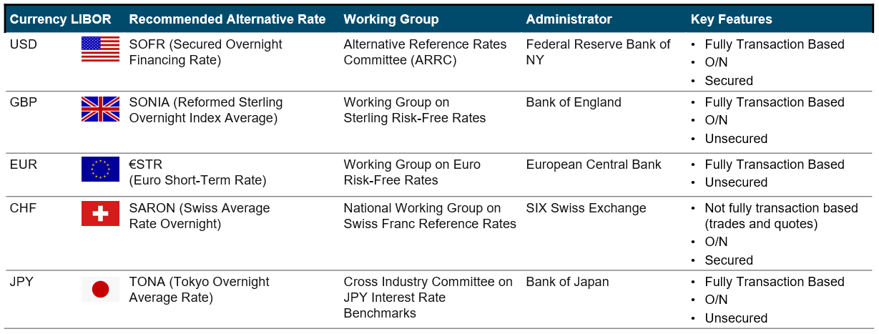

What alternative rates were recommended to replace LIBOR?

- USD: Alternative Reference Rates Committee (ARRC)

- GBP: Working Group on Sterling Risk-Free Rates

- EUR: Working Group on Euro Risk-Free Rates

- CHF: National Working Group on Swiss Franc Reference Rates

- JPY: Cross Industry Committee on JPY Interest Rate Benchmarks

How are SOFR/SONIA different from LIBOR?

SONIA, the recommended replacement rate for GBP LIBOR, measures the rate paid by banks on overnight funds. It is calculated as a trimmed means of rates paid on overnight unsecured wholesale funds. Per the Sterling RFR Working Group, SONIA is robust because it is anchored in active, liquid underlying markets. For more information on SONIA, click here.

Who are the relevant industry bodies, or Working Groups, providing guidance related to the transition?

What does the ARRC do?

What does the Working Group on Sterling Risk-Free Reference Rates do?

What is fallback language?

What is the timeline for the transition?

Other resources

The below resource links are not affiliated with SVB and are provided for information and educational purposes only. Any opinions and/or views expressed do not necessarily reflect the opinions and/or views of SVB.

Central Banks &

Working Groups:

US:

Federal Reserve Bank of New York (FRBNY) Alternative Reference Rate Committee (ARRC)

UK:

Bank of England Working Group on Sterling Risk Free Rates

EU:

European Central Bank (ECB) Working Group on Euro Risk Free Rates

SWITZERLAND:

Swiss National Bank National Working Group on Swiss Franc Reference Rates

JAPAN:

Bank of Japan (BOJ) Cross-Industry Committee on Japanese Yen Interest Rate Benchmarks

Industry Bodies:

International Swaps and Derivatives Association (ISDA)International Capital Market Association (ICMA)

UK Finance

Loan Market Association (LMA)

Loan Syndication and Trading Association (LSTA)

Asia Pacific Loan Market Association (APLMA)

Treasury Markets Association (TMA)

Japanese Bankers Association (JBA)

Official Sector:

Financial Stability Board (FSB)International Organization of Securities Commissions (IOSCO)

Financial Industry Regulatory Authority (FINRA)

U.S. Commodity Futures and Trading Commission (CFTC)

U.S. Securities and Exchange Commission (SEC)

U.K. Financial Conduct Authority (FCA)

Hong Kong Monetary Authority (HKMA)

Monetary Authority of Singapore (MAS)